Macro Matters: Focus Shift From Tariffs Back to Fundamentals

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

Key takeaways

- Growth: Global uncertainty gradually receding despite continued tariff negotiations

- Inflation: Tariff-induced U.S. inflation risk likely contained for now

- Rates: Central bank policies continue to diverge worldwide

Growth: Fundamentals show gradual U.S. slowdown versus some international stabilization

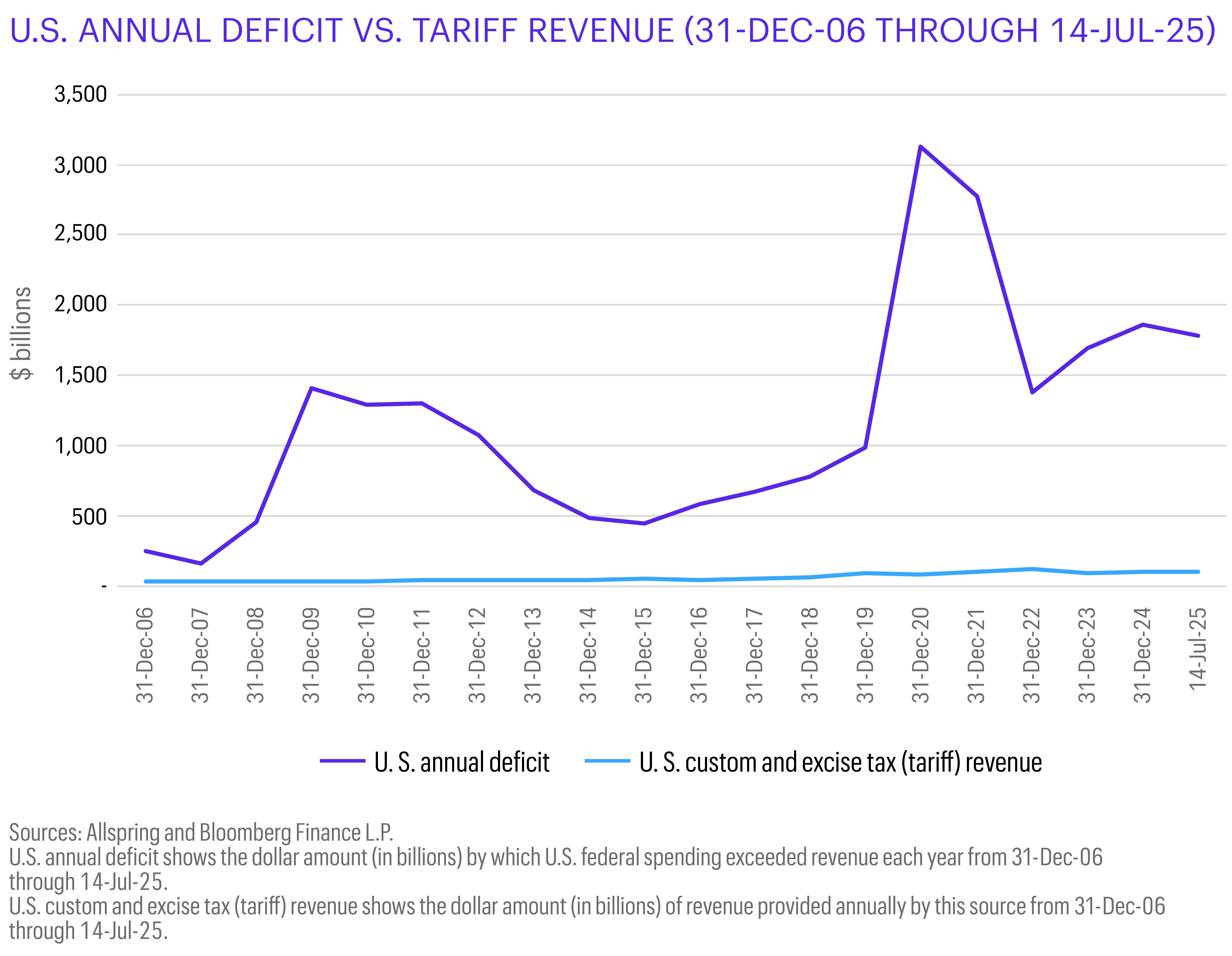

The U.S. economy remains resilient, with the Atlanta Federal Reserve (Fed) now projecting 1.4% growth in 2025. Consumer spending remains steady although discretionary sectors like restaurants and household goods are softening. June’s jobs report showed a 147,000 gain, a drop in unemployment to 4.1%, and moderating wage growth. Consumers will likely use the additional fiscal stimulus to boost their low savings rate. Business investment and the labor supply, however, could face pressure due to trade-policy uncertainty and a sharp immigration slowdown. The fiscal stimulus should help offset tariffs’ negative impact on growth over the short term, but it won’t be nearly enough to provide relief for the government debt dynamics overall (see chart below). Tariff negotiations will likely push out to August. We expect to see the focus decrease on regional tariffs and increase on sectoral tariffs, as they’re more impactful and easier to implement globally.

In the eurozone, 2025 growth is expected to stay below 1% amid weak demand and a manufacturing slump, especially in Germany and France. Still, sentiment indicators are improving, and fiscal support—including Germany’s tax cuts and the European Union’s infrastructure spending—may help recovery. Tariffs have begun inflating prices in certain sectors, like automobiles, and trade negotiations haven’t progressed enough to reduce them significantly.

China is targeting 5% growth in 2025, supported by rate cuts and infrastructure stimulus. However, structural challenges persist, such as declining demographics and weakening confidence. Trade tensions with the U.S. and Europe add more uncertainty and likely won’t disappear as China will be targeted through both direct and indirect tariffs.

Inflation: U.S. likely to remain sticky while international prices moderate

U.S. inflation ticked up 0.1% in May to 2.7%. The market expects it to remain stable, and consumers’ one-year-ahead expectations have declined. However, purchasing managers’ outlook, based on the Institute for Supply Management Prices Index, indicates that raw materials prices are expected to rise, which will likely mean rising prices for finished goods. Fed Chair Powell has reiterated a cautious stance, balancing inflation control with likely softening growth.

In the eurozone, inflation reached the European Central Bank’s (ECB’s) 2.0% target in June, supported by falling energy prices and a stronger euro. The ECB has continued cutting rates although growth concerns persist—second quarter growth is expected to be flat or slightly negative. Inflation in the U.K. rose to 3.8%, driven by services and food prices. The Bank of England (BoE) remains cautious given sticky inflation. In China, most prices remain deflated, reflecting weakness in real estate and consumer spending.

Rates: Fed likely comfortable on hold through summer

With tariff-related uncertainty and softening growth, the Fed remains cautiously on hold with the federal funds rate at 4.25–4.50%. While U.S. inflation has moderated, it’s still above the Fed’s 2.00% target and may increase short term due to higher import prices and a weaker dollar. The market’s rate-cut expectations for 2025 have dropped from four cuts down to two, and the Fed will likely remain on hold at least until September.

In the eurozone, the ECB has cut deposit rates by 2.00% since early 2024, down to the current 2.00%. With inflation near the region’s 2.00% target and growth still fragile, the ECB is expected to pause cuts after a possibly final move in September. In the U.K., the BoE has reduced rates to 4.25% from a 5.25% peak, with markets pricing in two more cuts by year-end. With inflation still above target at 3.4%, though, the BoE will likely proceed cautiously. In China, the People’s Bank of China (PBoC) has continued easing policy to counter deflation and weak domestic demand.

Implications for fixed income

U.S. tariffs are here to stay although bond markets will be increasingly affected by fundamentals. We expect U.S. growth will slow gradually and inflation will decline despite tariff uncertainties. Globally, yields remain attractive, and we believe international central banks will resume cutting interest rates after a summer pause.

We expect U.S. bonds will remain supported and earn the carry. Interest rates will likely continue falling on the short end of the curve, although probably not before the third quarter of 2025. Increased fiscal stimulus and a weaker U.S. dollar may lead to higher volatility in longer-maturity bonds, and we believe the interest rate curve will continue steepening as the market rebuilds a term premium into these bonds. We favor higher-quality U.S. bonds with low- to medium-term durations given they’re less affected by interest rate and growth volatility.

International bonds remain supported by lower growth and lower inflation, although these are largely priced in already. We’ll need to see the full effects of the fiscal stimulus from defense and infrastructure spending and whether they drive up personal consumption. While we’re positive on international bonds for now, we’d focus on short- to medium-term maturities.

Implications for equities

We remain constructive on international equities, including emerging markets, and on cheaper sectors of the U.S. market. We expect tariff negotiations will eventually settle and markets will refocus on fundamentals. Second quarter earnings will be scrutinized given April’s extensive trade-induced uncertainty. We believe that potentially lower geopolitical risk, more fiscal spending, and anticipated looser monetary policy—including in the U.S.—should support equities in the second half of 2025. Focusing on quality and valuation remains a prudent approach for us.

Implications for multi-asset portfolios

Within global equities, our outlook is optimistic particularly for European, emerging market, and Chinese equities, where valuations remain attractive and both monetary and fiscal policies are supportive. These markets offer diversification benefits and are well positioned to benefit from easing cycles by the ECB, BoE, and PBoC. In the U.S., we expect the Fed will eventually pivot toward supporting growth to bolster equity sentiment, especially in rate-sensitive sectors.

We continue to like bonds over cash. In the U.S., we believe the interest rate curve has more room to steepen. With the Fed expected to gradually shift from inflation to growth concerns in the second half of 2025, U.S. equities could benefit from lower interest rates, fiscal stimulus, and perhaps lessening concern over tariffs—although tariffs do have the potential to create short-term uncertainties. We also see further weakness ahead for the U.S. dollar, which reinforces our desire to overweight gold as it can benefit from a weaker dollar, lower real yields, and persistent geopolitical uncertainty.

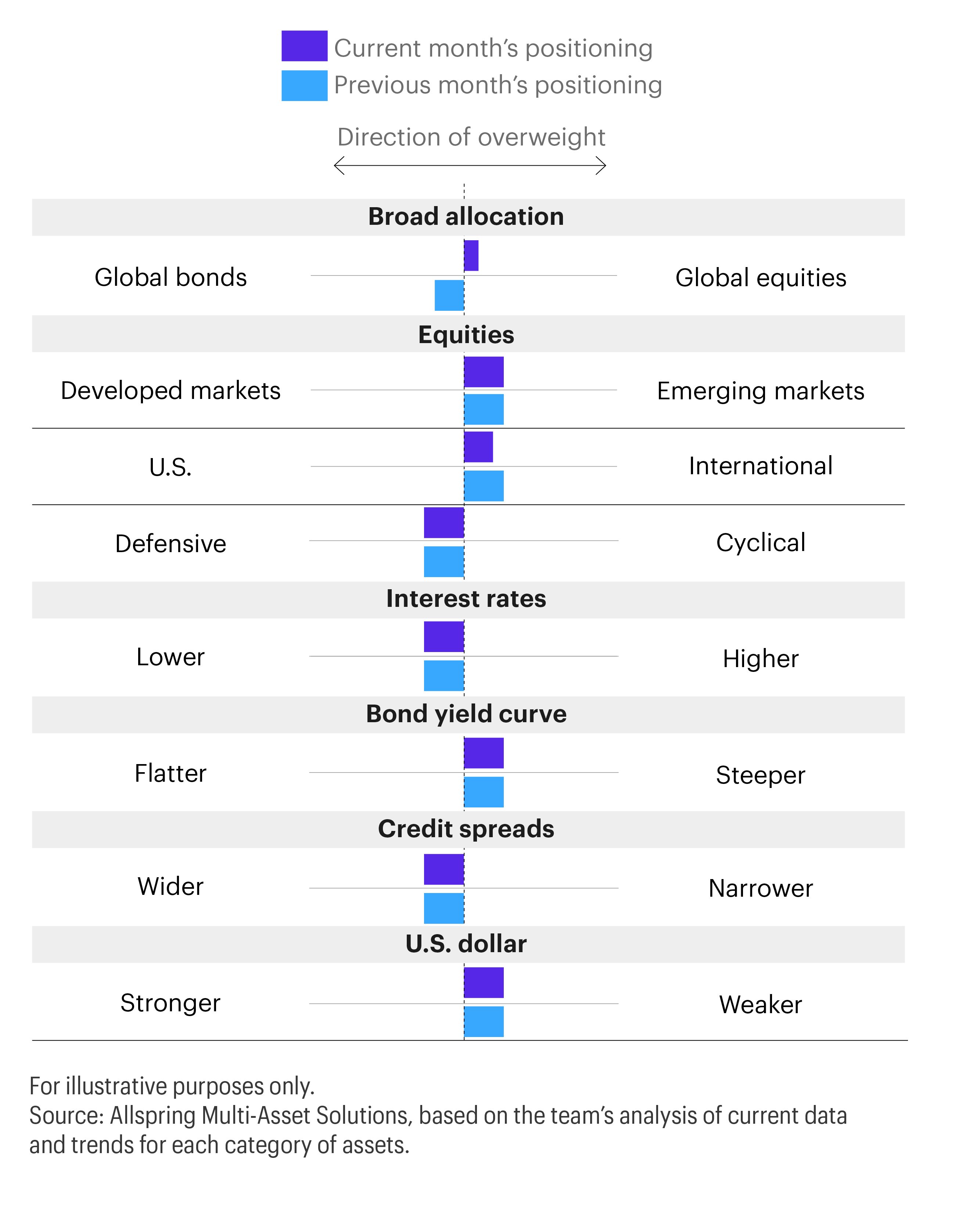

Potential allocations based on today’s environment

The table below depicts our views on short-term trends. These perspectives are developed using quantitative analysis of data over the past 30 years overlaid with qualitative analysis by Allspring investment professionals. The positioning of each bar in the table shows the direction and magnitude of an overweight.

ALL-07142025-qbdl0qxe

Related insights

George Bory and Ann Miletti share Allspring's 2026 outlook. From resilient bond strategies to AI-powered equity growth, they unpack the key drivers set to shape next year's financial markets.

Which macroeconomic trends do we think matter the most? Read this month’s issue of Macro Matters.

Article

Nothing to See HereDespite limited access to reliable data due to the ongoing government shutdown, the Federal Open Market Committee (FOMC) announced another 0.25% cut, lowering its key interest rate to 3.75–4.00%.

How are Allspring’s investment experts thinking about the U.S. government shutdown and market implications?

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

The Federal Reserve lowered its key rate by 25 basis points at its September meeting following an eight-month pause. George Bory and John Campbell discuss how U.S. bond and equity markets could respond.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

With a robust U.S. economy, above-target inflation, and continued tariff uncertainty, the FOMC kept its key interest rate at 4.25–4.50%.

Speculation over the next chair of the Federal Reserve (Fed) is dominating headlines and keeping markets on edge. A more dovish leader could mean a big shift in monetary policy and raise concerns about the Fed’s independence.

As the events concerning Iran continue, Allspring Fixed Income’s message—"bonds provide certainty in an uncertain world”—remains central to our positioning.

A potential conflict with Iran has consistently appeared in our monthly Market Risk Monitor for over two years. Now that risk has materialized. Our equity portfolio managers assess the implications for global markets.

What might the future hold for markets? In this roundtable discussion, our investment experts explore pressing topics like deficit spending, trade tensions, the Fed’s next moves, and the weakening U.S. dollar.

With ongoing tariff uncertainty and U.S. employment still strong, the Fed kept its key interest rate at 4.25–4.50%.

Amid uncertainty around tariffs and their impact on U.S. growth and inflation, the Federal Reserve held its key interest rate at 4.25–4.50%. We explain what may lie ahead.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

George Bory discusses three key U.S. headlines from April 22 and how fixed income assets may be affected.

George Bory discusses reasons for the recent sharp price fluctuations in stock & bond markets, including in U.S. Treasuries, and identifies actionable approaches fixed income investors may pursue in today’s environment.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

Article

Tariffs: A New NormalPresident Trump announced specific details on the administration’s intended trade policy, including a baseline tariff as well as reciprocal tariffs on specific countries. Uncertainty lies ahead as global markets digest the prospects.

At its March meeting today, the Fed kept the federal funds rate at 4.25–4.50% amid concerns around tariffs and their potential impact on U.S. growth and inflation.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

The U.S. announced tariffs on Canada, Mexico, and China. Although tariffs on NAFTA countries are temporarily on hold, China is responding with its own retaliatory measures. Allspring experts discuss how these ongoing developments create uncertainty but also opportunities for active portfolio management.